Powered land has emerged as a critical asset class in data centre development. In this three part series, we explore some of the key legal, commercial and regulatory considerations shaping powered land transactions.

In the first article, we examine how powered land is emerging as a distinct asset class, where – beyond proximity to demand – access to reliable, near-term power is the principal driver of land value.

The second article explores power policy and regulation, planning and permitting, and how powered land values vary across different use cases.

The third article looks at how data centre developers are increasingly turning to co-located power solutions and private-wire networks to reduce reliance on congested national and regional grids.

The rise of data centre powered land strategies

An estimated 40,000 acres of land is required globally for data centre development in the next five years1. That’s around three Manhattan islands, or nearly half an Isle of Wight. Land itself is not enough: the second crucial ingredient is power. Powered land – broadly, a plot with a grid connection – has become a valuable commodity. We are seeing increasing market activity: logistics operators reappraising their land banks; investors adopting powered land as a strategy in its own right, as well as developers of energy generation, distribution and storage projects considering whether the sites they hold have data centre potential.

What, then, are the key considerations when making a powered land data centre play? Location and power are the most important, but not all land is equal – certain locations will be viable for data centre development, others will not.

Location

As a starting point, data centres are situated in proximity to end users: latency sensitive workloads such as enterprise IT, financial services and content delivery must be sited close to the businesses and populations they serve. In the US, this has produced a cluster of dominant primary markets: Northern Virginia’s ‘Data Centre Alley’ (the largest data centre market in the world); Chicago, Dallas-Fort Worth, Texas; and Silicon Valley – each proximate to dense concentrations of enterprise and government demand. The primary European data centre locations are the so-called ‘FLAPD’ of Frankfurt, London, Amsterdam, Paris and Dublin. However, severe capacity constraints in these primary markets are pushing demand outwards: Madrid and Milan, for example, are benefitting from FLAPD spillover as operators and occupiers seek available power and suitable sites.

A distinct category of use case, however, is far less sensitive to latency and therefore to proximity to population centres. Hyperscale cloud infrastructure, high-performance computing, and AI model training are all extraordinarily power-intensive workloads. For these uses, it is the availability of cheap, abundant power rather than location relative to end users, that primarily drives their siting. The Nordics have emerged as a leading destination for exactly this reason: plentiful renewable electricity (predominantly hydropower and wind), sub-zero ambient temperatures that dramatically reduce cooling costs, and strong renewable energy credentials that satisfy corporate ESG commitments. These characteristics allow operators to site large facilities in relatively remote locations. More broadly, the availability and cost of power, resilience of local supply chains, regulatory environment, and proximity to end users all bear on location decisions, each weighted differently depending on the use case in question.

The UK illustrates these dynamics well. For example, Scotland has significant renewable energy resources, but the infrastructure required to transmit that power to areas of high demand in the UK remains a limiting factor. This creates opportunities for investment in both the land situated close to renewable energy sources, where power is cheap and available, and in battery storage technology. Battery storage can capture supply and help mitigate the intermittency inherent in renewable energy production.

For the plot of land itself, all the usual considerations for a real estate investment apply. Land rights and ownership are fundamental and require local expertise. Understanding what it means to hold a hereditary building right in Germany or benefit from a usufruct in France is crucial. Even if the freehold of the land is owned, careful diligence is required to determine the rights from which it benefits, and the obligations and covenants to which it is subject. If the land is part of an industrial area, is the owner required to join a management company and contribute to an estate service charge? Does a neighbour have a right to use a shared accessway? A grid connection may be in place with a power company, but does the landowner have the right to lay and maintain the necessary cables, or will third party consents be required? Does the site have local access to multiple fibre backbone connection points? Where multiple buildings are intended on a single plot, it is usually a good idea to consider at the outset how the land can be subdivided to facilitate future disposals of one or more stabilised assets.

Power

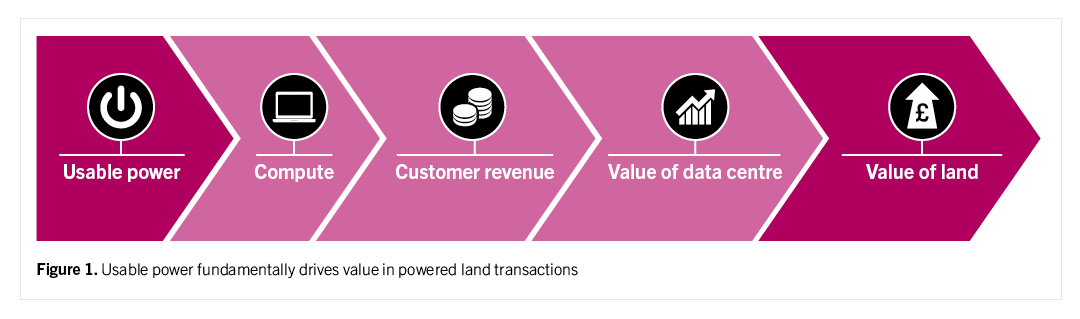

The value in the land is tied to the data centre that is going to be built on it. The value in that data centre is derived from the expected customer revenue, which in turn is dependent on compute, itself a function of available usable power. Understanding the usable power is therefore crucial in any data centre investment opportunity (please see Figure 1 below).

A contractual right to power is what characterises a powered land opportunity, however, the nature and terms of those arrangements vary considerably and require close scrutiny. In this article, we are primarily concerned with standard grid connection arrangements to the distribution/transmission network. In the third article, we will go on to consider more bespoke “private wire” grid connection arrangements.

For these purposes, there are two key forms of energy contract: grid connection agreements and power purchase agreements (PPAs). The former establishes a right to connect to the grid with the owner of the electricity infrastructure; the latter governs the ongoing supply of energy by an electricity provider to an end-user.

Key diligence points for grid connection agreements will relate to the capacity, timing and certainty of delivery as well as grid availability and the risk of grid outages. The agreement should specify the maximum power capacity (usually in megawatts) that the grid operator will supply to the land, and the works (and costs) required to deliver this power to the site. This will determine the eventual capacity of the operating data centre and, in turn, drive the value of the site. Similar rigour should be applied to any PPA, to understand the quantity of contracted electricity (and the profile of any initial “ramp-up” of delivery), the pricing mechanism, duration and key payment terms.

Understanding the physical delivery of power to the site is as important as the legal framework – whether it is underground, overground, whether a new substation is required, the procurement process and timeline for that infrastructure.

The ramp-up of grid connectivity, as well as subsequent reduced grid availability due to outages, can lead to power supply issues. Are there going to be interruptions to supply whilst phased grid connection works or grid reinforcement works are being undertaken and is there sufficient redundancy in the grid to continue operations, perhaps at reduced power? This needs to be assessed upfront to understand whether there will be frequent downtime and how that will affect customer revenue/credits. Where there is downtime, that will sometimes be supported by back-up generators, which are often fossil fuel powered to deliver sufficient cooling. Investors will want to factor into the business plan the additional cost of this as well as any limitations on running generators round the clock imposed by local environmental rules.

When factoring a headline MW into any land valuation or development appraisal, it is also important to understand how “committed” the committed power really is. Grid network operators will be hesitant to be on the hook for this – there is little commercial incentive to accept any material liability for a failure to deliver promised grid connections on time or for subsequent grid outages. Delivering the required grid connection is increasingly likely to be contingent on wider upgrades to the network infrastructure – higher capacity cabling, new routing, a new substation etc. These matters are all outside of the control of the landowner. This often leads to a degree of risk-sharing between a powered land owner and any third-party capital provider: what if the power is delayed, or does not come online at all? Deferred or contingent consideration and clawback mechanisms can be used to allocate risk accordingly.

Power commitment can be a two-way street: in Part 2 we will also look at so-called ‘use-it-or-lose-it’ (UIOLO) regimes, becoming common across Europe as a means of managing the allocation of capacity and avoiding ‘land banking’, and what these rules can mean for a powered land investor.

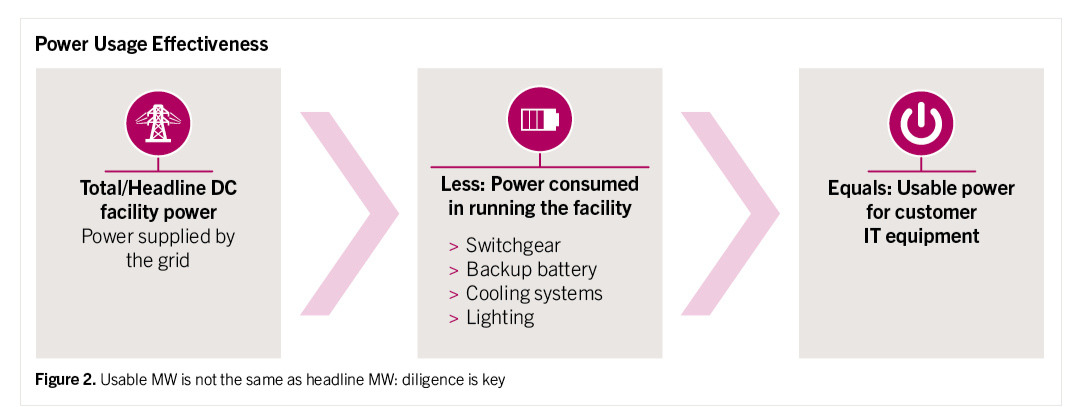

Power Usage Effectiveness (PUE)

Headline committed megawattage does not translate directly into usable data centre capacity. A detailed, technical understanding of the planned data centre operation – and in particular cooling – is required to calculate the expected usable megawattage. This power usage effectiveness (PUE) will need to be assessed by technical experts before any valuation is agreed by a potential investor/buyer. A good rule of thumb for desktop purposes would be to assume a PUE of 1.5, meaning you can expect a loss of 1/3 between utility power (what arrives on site) and IT capacity (the power that can actually be monetised through customer revenue).

Fibre connectivity

For cloud and enterprise deployments, proximity to dense metro fibre networks and user demand centres remains essential, as low latency and access to internet exchanges are key. For large-scale AI training deployments, location is typically less constrained by metro proximity and more driven by power and land availability, although access to high-capacity long-haul or backbone fibre and robust backhaul remains essential. In all cases, a specialist telecoms adviser will assess the site’s proximity to existing fibre infrastructure, the availability of sufficient capacity, and, crucially, the presence of multiple diverse routes to ensure resilience.

Fibre delivery to the site is typically led by the carrier or network operator, who will design and extend their network to the site boundary (often securing any required wayleaves or easements), although in more remote locations this may require some level of developer coordination or contribution.

On-site connectivity infrastructure, such as ducting and building entry, is usually delivered by the developer in coordination with the carrier. Hyperscale tenants will strongly influence technical requirements and carrier selection, but do not typically deliver the infrastructure themselves. Overall, provided a site is located within reasonable proximity of existing networks and has credible options for resilient routing, fibre is generally considered a manageable and lower-risk workstream than power, albeit one that still requires careful diligence around capacity and route diversity.

1 Hines Research, 2025

Written by Peter McCabe and Jack Shand.

A selection of our key experience:

IREN

on its acquisition of Nostrum Group in Spain, securing c.490MW of powered land and establishing its European platform for AI data centre development.

CPP Investments and Equinix

on US$4 billion acquisition of atNorth.

CPP Investments

on an €8 billion European data centre partnership with Goodman Group to develop a portfolio of data centre projects in Frankfurt, Amsterdam and Paris.

DigitalBridge and Vantage Data Centers

on a €1.4bn multi investor investment and platform re organisation of the Vantage Data Centers’ EMEA hyperscale data centre portfolio.

Digital Realty

on the acquisition of its first data centre site in Lisbon, securing powered land with redevelopment potential to deliver up to 2.4MW of IT load.

DigitalBridge

on the disposal by Yondr Data Centres of its interest in the power secured Yondr Malaysia data centre platform to Vantage Data Centers.

BlackRock

on the formation of the £500m Gravity Edge data centre platform with Digital Gravity Partners, focused on acquiring and developing power secured data centre real estate across the UK and Europe.

A financial advisor

on an acquisition of a US hyperscale data centre campus site in Chicago, with closing contingent on securing a 600 MVA grid connection and key real estate and permitting approvals.